Reed Steiner

Reed Steiner

Customers have grown so warry of cash and card readers that contactless payment apps, like Apple Pay, Google Pay, and Paypal, are crawling from the grave. But is this a temporary bubble, or are NFC touchless payments here to stay?

Touchless Payments Before COVID-19

Back in 2019, we all knew that contactless payments were the future. They just…hadn’t been growing as much as we’d have hope.

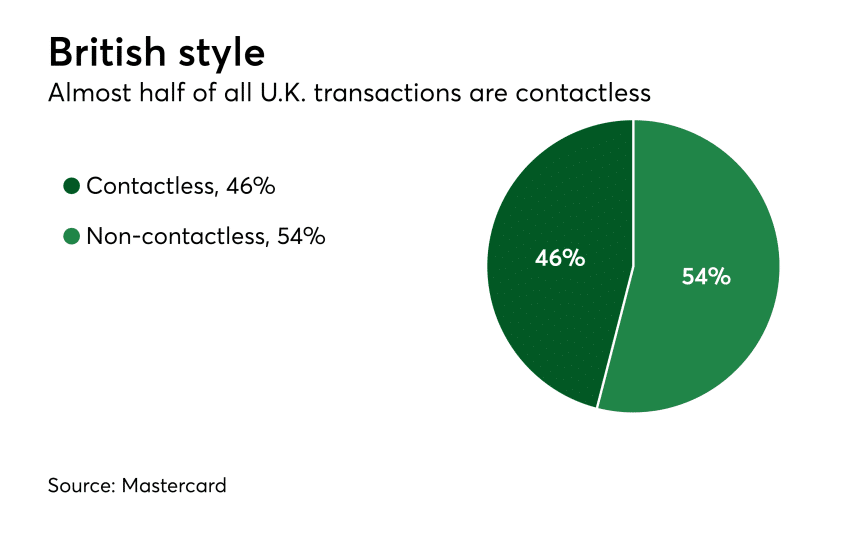

This problem was uniquely American. The UK, for instance, has accepted contactless payments with open arms. In fact, nearly half of all in-store transactions use contactless payments.

So what’s up with the US? Why did it take a pandemic to adapt NFC contactless payments?

Well, US retailers are just slow–very slow. It took a Target security breach for retailers to shift from the magnetic strip to the chip, and now, it’s taking a pandemic to toward contactless payments.

However, just before the pandemic, we were already starting to see major shifts toward contactless payments. The Visa Earnings Report explains that even though the US is abysmally behind the rest of the world, many huge brands, such as 7-Eleven, CVS, and Costco, were beginning to adapt the technology into the end of 2019. New York’s Metropolitan Transit Authority even began to roll out OMNY, a contactless transit fare system, at the end of 2019.

Here’s the takeaway: though the US has been way behind every other country, we’ve spent the past year integrating the technology into every facet of in-person purchases. All we needed to get the ball rolling was a push down the ramp.

How the Touchless Takeoff Began

No one should be surprised that contactless payments are taking off. In fact, the CDC explicitly recommends touchless payment whenever possible:

- Encourage customers to use touchless payment options, when available. Minimize handling cash, credit cards, reward cards, and mobile devices, where possible.

Even when contactless payments aren’t possible, handling money has become a huge hassle.

- When exchanging paper and coin money:

- Do not touch your face afterward.

- Ask customers to place cash on the counter rather than directly into your hand.

- Place money directly on the counter when providing change back to customers.

- Wipe counter between each customer at checkout.

Every ethical essential-business owner should, if possible, adapt contactless payments to keep customers safe. COVID-19 threatens our most vulnerable loved ones, so it’s our duty to do everything we can to flatten the curve. We’re already seeing the impacts. A whopping 27% of surveyed businesses in the US have seen an uptick in contactless payments, and that number will only continue to grow.

But the CDC was only the beginning of the Touchless Takeoff. Of course, everyone is afraid to use cash, and that fear is completely valid. But fear alone can’t combat America’s poor contactless infrastructure. After all, if stores don’t accept Apple Pay, how will people use touchless payments?

No, this boom runs much deeper than the pandemic. The true takeoff began with the retailers.

3…2…1…We Have Liftoff: How Retailers Sustained the Touchless Takeoff

Sure, no one wants to handle money. That rational safety concern is enough to fuel a touchless boom. But that boom wouldn’t last if it weren’t for the speed at which retailers adapted to customer demands.

Grocery Giants

It all starts with Walmart.

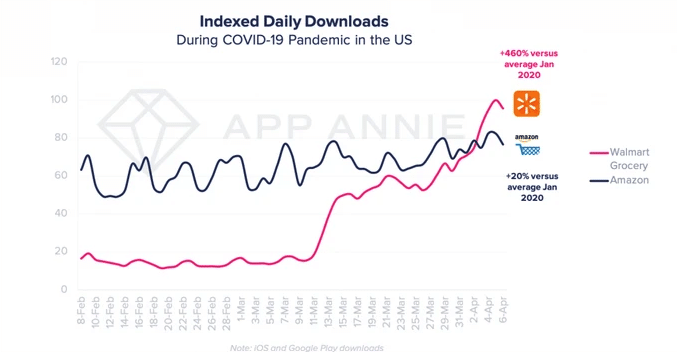

Walmart did not plan for the Walmart Grocery app to explode. In fact, as late as March 2020, they planned to merge it with their primary app. Again, Coronavirus changed that. Customers made the smart decision to grocery shop online, which propelled Walmart Grocery to the top of the charts. By April 5, it was number 1 in the Shopping category, passing Amazon by 20%.

You will notice two spikes on the graph. The first spike occurs on March 11, when the WHO classified COVID-19 as a pandemic. The second spike occurs on March 27, when Walmart announced contactless payments.

Contactless payments pushed Walmart Grocery past Amazon.

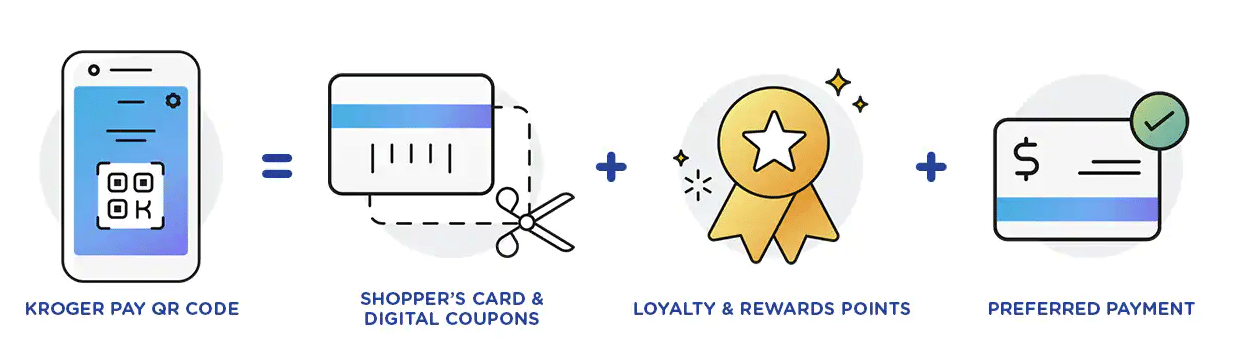

If the CDC and WHO weren’t enough to make grocery stores go contactless, that level of success was. Shortly after Walmart’s monumental success, Publix, the Florida-based grocery and pharmacy chain, announced a new contactless feature on its own app. Even chains that have held out against Apple Pay have adapted contactless payments. While Kroger and Fry’s still refuse Apple Pay (locations may vary), they continue to push Kroger Pay as an alternative in response to the crisis.

Clearly, contactless payment is here to stay in the grocery industry. While grocery chains may continue to resist Apple pay, their in-app contactless payment systems have exploded in popularity and driven unprecedented downloads of each company’s apps. Touchless payments aren’t leaving the grocery industry any time soon–but what about restaurants?

Touchless Payments in Restaurants

Unfortunately, restaurants have taken a major blow during this crisis. However, contactless deliveries are helping many restaurants adapt.

For big restaurants, contactless payments are easy. Burger King could easily integrate contactless payments into their existing application.

Smaller restaurants have things a lot rougher. Most small restaurants don’t have apps–or the revenue to develop one. However, those that use existing eCommerce solutions can still adapt to changing times. Sellers using Square now have access to curbside pickup and local contactless delivery.

Today we're releasing curbside pickup, and adding a local delivery feature that will be available later this week.

We are also waiving curbside pickup and delivery fees for the next 3 months. We already offer online orders for in-store pickup with no monthly fee.

2/

— Square (@Square) March 18, 2020

Even old school restaurants are reaping the benefits of contactless payments thanks to Uber Eats Leave at Door Deliveries. As long as Uber Eats and other delivery apps continue to promote contactless deliveries, touchless payments will continue to soar.

Note that contactless payments aren’t going to save small restaurants, which are taking a major hit. Do everything you can to support your local restaurants–and use contactless payment whenever possible.

Nevertheless, touchless payments and contactless deliveries are helping many small restaurants stay afloat. But what about the fintech apps themselves? What’s changed with apps like Apple Pay, Google Pay, and PayPal?

Touchless Fintech Apps

Kroger and other grocery chains may resist Apple Pay in favor of their own apps, but that hardly means that Apple Pay, Google Pay, and other contactless payment apps got the short end of the stick. In fact, this touchless takeoff has benefited contactless payment apps more than any other company.

The clear victor for contactless payments is PayPal, thanks to the stimulus checks. Users with a PayPal Cash Plus account can cash their stimulus check for free. Not only does this campaign get the stimulus check into the pockets of more Americans who may not have had any other means to cash the check, it also boosts the number of PayPal Cash Plus accounts. Clearly, that’s great news for PayPal, since it gives them a huge edge.

However, ApplePay is likely to grow the most. An eMarketer forecast predicts that Apple Pay will control a whopping 47% of the American mobile payment market. Plus, Apple just struck a deal with UBS, putting an end to their feud with Swiss companies like Twint. ApplePay will continue to grow tremendously, and it shows no sign of stopping after the pandemic. Once people make the switch, why would they switch back?

What Does This Boom Mean for Apps with Contactless Payments?

These are unprecedented times, so it’s impossible to predict for sure what’s going to happen. Every industry is different.

However, contactless payments were growing before the pandemic and will certainly continue to grow after it. Whether you run a small Shopify POS store or a multinational retail chain, do everything you can to support contactless payments. If you have an app or are considering developing one, consider whether contactless payments are right for your users.